Markets don't like uncertainty - and right now there is plenty of it. Conflict in the Middle East, questions over oil supplies and renewed tariff tensions have all tested investor confidence. We explain why we remain broadly positive about the outlook despite these pressures and what actions we have already taken to protect our clients’ portfolios. We believe our focus on quality and diversification is the right approach for times like these.

What the conflict means for markets

US and Israeli military action against Iran has cast doubt on growth expectations for the coming year. Market volatility has increased as investors reposition portfolios amid disruptions to global oil and gas supplies and to broader shipping container traffic through the Strait of Hormuz. It is a vital shipping lane; around 20% of global oil supplies are transported through the region. If oil and gas prices remain high for an extended period, this would put upward pressure on inflation, throwing into question expectations for the timing and magnitude of interest rate cuts. It may also affect consumer spending, as higher energy bills weigh on disposable incomes.

Of course, a great deal hinges on the duration of the conflict. A short, effective US-Israeli campaign could quickly see energy prices return to pre-conflict levels. However, any escalation that leads to an extended closure of the Strait of Hormuz could materially reduce global growth estimates. Before the conflict, the global economy was expected to grow by more than 3% in 2026, broadly in line with last year, supported by several factors. Lower interest rates in the US, the UK and Europe have eased the burden of borrowing costs for consumers and businesses. At the same time, governments are spending more on infrastructure and defence, which will boost their economies. Even with the additional risks arising from recent events in the Middle East, on balance we view the economic environment as generally supportive for companies, and our broadly diversified portfolios as being well-positioned to protect against the worst of any market setbacks.

How we’ve positioned portfolios

Towards the end of last year, we increased the equity exposure in our clients’ balanced portfolios from 65% to 70% (the historic range has been 55%-80%). We carefully selected which positions to build and which to trim for profit, to increase diversification. Our rationale for doing so was straightforward. Valuations had become stretched amongst AI-related companies, contributing to acute market concentration amongst a small number of large US technology stocks. We felt markets were primed to broaden out and away from the AI-trade, into different sectors and geographies.

We felt markets were primed to broaden out and away from the AI-trade, into different sectors and geographies.

As a result of investors’ focus on one sector and a few companies, we identified attractively valued businesses, recently overlooked and perhaps less fashionable, in other parts of the market that offer more reliable returns and dividends. Accordingly, we took profits in stocks that had benefited from AI-related exuberance and added to companies with more attractive valuations and predictable income streams. The companies we have added to trade on an average forward price-to-earnings multiple of 18.7x, well below the global index, which currently trades at an average multiple of 22x*. (Note: Price-to-earnings is a common measure of stock valuations.)

Aside from being well-positioned to benefit from the broadly supportive economic outlook, their stable earnings growth, reasonable valuations, and dividend income should support their valuations even when broader markets are affected by abrupt swings in investor sentiment.

Overall, we believe that a high-quality, diversified portfolio provides the most appropriate platform for growth and protection of clients’ capital over the long term, including many scenarios that may unfold from here.

Overall, we believe that a high-quality, diversified portfolio provides the most appropriate platform for growth and protection of clients’ capital over the long term, including many scenarios that may unfold from here.

Why we prefer high-quality companies and broadly diversified portfolios

Our equity selection focuses on a broadly diversified portfolio of high-quality companies. This is evidenced in the tables below. Table 1 compares the geographic diversification of McInroy & Wood’s (MW) core balanced strategy (as reflected in the Balanced Fund), to the global equity index (as reflected by the MSCI All Country World Index). We do not make any reference to this index when managing these strategies.

Still, the comparison highlights that our portfolios are significantly more diversified, positioning them well for an unwinding of the historically high concentration of global markets in US companies. History shows that this level of concentration is unlikely to persist.

Table 1 – Greater diversification**

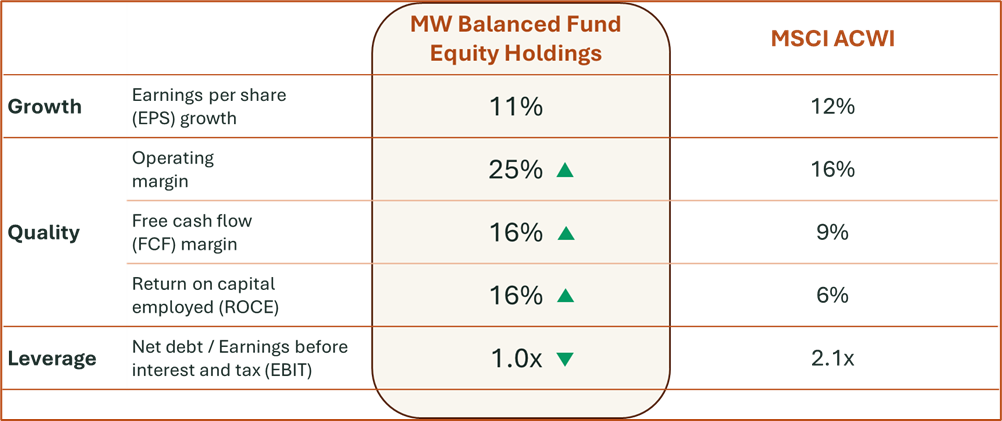

The relative quality of the companies MW invests in is shown in Table 2. This compares the key financial metrics of the Balanced Fund's equity holdings to those of the global equity index at a specific point in time. These quality stocks have generally been out of favour in recent years, while high-growth stocks and momentum strategies have propelled markets to new highs. The strong operational performance of our preferred companies has not been adequately reflected in their share prices, as investors have focused elsewhere. This is one of the key contributors to MW portfolios lagging the wider market during the concentrated US-tech-driven rally.

Table 2 – A quality portfolio

The metrics shown represent characteristics of average equity holdings within the relevant fund / index and not the performance of the fund or index itself or any specific portfolios or equities. These metrics should not be considered in isolation. They represent only selected financial characteristics and do not provide a complete basis for investment decisions. The comparison with the MSCI ACWI is provided for context only and may not represent a like for like.

As the table shows, the companies we prefer to invest in earn above-average profits, generate substantial free cash flow, and reinvest that cash internally at higher-than-average rates of return in projects that grow or improve the business. They can do so because they typically occupy commanding market positions. Given these characteristics, high-quality companies tend to perform well across a wide range of market conditions. For this reason, we are confident that the enduring appeal of high-quality stocks will win back investors’ affections in due course.

Outlook:

As ever, the outlook for markets is balanced, with reasons to be positive and obvious reasons for caution. President Trump has reintroduced tariff uncertainty following a Supreme Court ruling that his trade policies exceeded his executive powers. Renewed uncertainty has been created by replacing previously negotiated tariffs with a global rate of 15%, albeit for only 150 days. Meanwhile, Trump’s rhetoric over Greenland has upended the geopolitical order, prompting Mark Carney to issue an eloquent rallying cry to the so-called “middle powers”. And, of course, US-Israeli action against Iran has called into question the outlook for energy prices, inflation, and interest rates. We believe broadly diversified portfolios, like those we manage for our clients, are well-positioned to withstand the uncertainty and inevitable market volatility this conflict will create. Moreover, if the conflict has a short-lived effect on energy prices, we expect markets to recover any ground lost.

After a full year of Trump’s second term as president, the global trading system has proven flexible enough to adapt to his unpredictable protectionist policymaking. Not only has global economic growth remained resilient, but inflation and interest rates were on a supportive trajectory before the recent events in the Middle East. As we look further ahead, an unparalleled boost in productivity may be on the horizon as AI becomes increasingly embedded in our daily lives. Overall, there are still many reasons to be positive about the future.

*As at 16th Feb 2026

**Source: Bloomberg. Average figures for equities held in the Balanced Fund and MSCI ACWI. Data accurate as at 15 January 2026. Past performance is not a guide to future performance.

Past performance is not a guide to future performance. The value of shares / units and the income from them can go down as well as up and you may not get back the full amount originally invested.

The views expressed in this document are not intended as an offer or solicitation for the purchase or sale of any investment or financial instrument, including in relation to any of McInroy & Wood’s funds. The information contained in this document does not constitute investment research, investment advice or a personal recommendation and should not be used as the basis of any investment decision. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. This article does not take account of any potential client’s investment objectives, particular needs or financial situation.

This article reflects McInroy & Wood’s opinions at the date of publication only, the opinions are subject to change without notice, and McInroy & Wood shall bear no liability for any loss arising from reliance on it.

This financial promotion is issued by McInroy & Wood Limited, which is authorised and regulated by the Financial Conduct Authority.

Markets don't like uncertainty - and right now there is plenty of it. Conflict in the Middle East, questions over oil supplies and renewed tariff tensions have all tested investor confidence. How are our clients’ portfolios positioned for this environment, any why?

ESG investing and the energy transition have failed to reduce global carbon emissions over the last decade. What factors have slowed the energy transition? And how should investors prepare for the next ten years?

Doing the right thing in investment markets usually feels unpalatable. Finding value often means swimming against the tide and hunting for ideas where others are not.