We recently hosted a talk in London with Lieutenant General Sir Nick Borton, senior NATO adviser. He shared frontline insights on the evolving nature of conflict, NATO’s shifting role, and the strategic challenges ahead. In this article, we reflect on his key points and consider their implications from an investment perspective.

Many investors look for changes in economies and markets to determine where to move next. Like a game of chess, investors attempt to think a few moves ahead and are well aware that equity and bond markets are dynamic pricing mechanisms, anticipating the effect of policy changes taken now.

When we look to recent years, significant returns were made by following the vast fiscal stimulus injected into the US economy by President Biden via the Inflation Reduction Act and Infrastructure Act, among others. It is this stimulus that has set US returns apart from the rest.

As the US wrestles with political change and shifts from a fiscally driven economy towards a more free-market approach, shaped by Republican ideology, we may need to look elsewhere for leadership and for change.

With inflation easing and interest rates continuing to fall in the UK and Europe, the balance is beginning to shift in favour of consumers and businesses – there is now clear light at the end of the tunnel following years of struggle with COVID, the invasion of Ukraine and elevated inflation. The relentless pressure from Chinese competitiveness and the more recent need to boost defence spending has driven European countries into action.

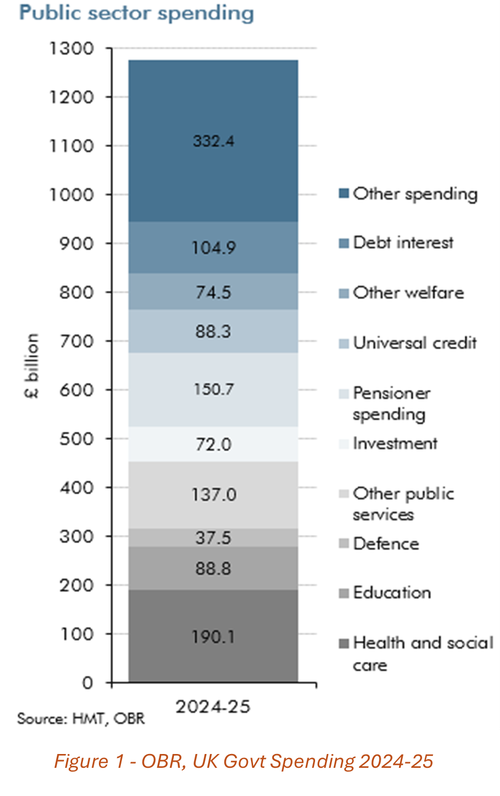

Figure 1 from the 2024–2025 OBR report highlights the opportunity. UK defence spending is running at just under £40bn, meaning that to raise this by even a few percentage points makes for a large number in absolute terms. When we add the announced spending increases in Germany – coming from a lower base – such numbers improve the outlook further.

Many of these points were brought into focus at a recent talk organised by our London office, by Lieutenant General Sir Nick Borton, former Commander of NATO’s Allied Rapid Reaction Corps, and now senior advisor to NATO.

While we see conflict and potential flashpoints in numerous places, these have been building over time, and it is perhaps complacency that now necessitates action.

He began by noting that today’s geopolitical environment is more dangerous than at any point in his service – perhaps even more so than during the Cuban Missile Crisis. The world has entered what he called “Globalisation 2.0”, a shift from the liberal, rules-based order of the post-WWII era to a fragmented, multipolar world marked by strategic competition and rising nationalism.

From the war in Ukraine to tensions over Taiwan and the more recent flare-up between the United States and Iran, the pattern is clear: geopolitical risks are no longer isolated events, but part of a broader shift in the global order.

US-led free trade and economic interdependence have delivered nearly 75 years of relative peace, which is now being undermined by tensions arising from deindustrialisation in the West, China’s rise outside liberal norms, monopolies over critical resources, and technological dependencies.

Russia’s strategic posture and Putin’s regime are fundamentally hostile to Western democracy, and General Borton was quick to dismiss the idea that NATO provoked Russia, noting that Moscow only began objecting to NATO expansion around 2008, when it became politically useful for Putin. Despite the Russian Army’s setbacks in Ukraine, it has proven more resilient and capable than many anticipated.

Russia has shifted to a war economy, with 7% of GDP and 40% of government spending now directed toward defence – underlining the seriousness of its long-term strategic intentions. In addition to more traditional foes, new threats are emerging from digital disruption, social media, political mistrust, and even nuclear proliferation and its safeguards.

The outcome in Ukraine will be crucial. A Russian victory or favourable peace deal would embolden autocrats worldwide. General Borton warned against the complacency of underestimating Russia’s long-term capacity to regroup and rearm. Russia, China, North Korea and Iran form a strategic axis that must be confronted collectively.

While NATO has been a cornerstone of Western security for 75 years, there is concern regarding the US’s wavering commitment – particularly under the Trump administration. General Borton indicated while US military contacts do not expect a full US withdrawal from NATO, it is clear Europe must prepare to shoulder more of its own defence burden, especially as US troop levels and capabilities on the continent may decline.

There are signs of a European defence renaissance. Northern and Eastern European countries – especially the Baltics and Poland – are increasing defence spending significantly. Germany has also announced a major investment package, potentially reversing decades of military underfunding and reliance on the US.

Positively, General Borton highlighted that Europe has the wealth, technology, and population to defend itself, but must act in a coordinated and strategic way with smarter spending, better readiness, and a unified approach to defence procurement and planning.

The issues almost read like an indictment of all that may have gone wrong with UK industry in recent years. The UK’s recent Strategic Defence Review takes a significant step to redress this, giving far greater support to step up government backing and spending. Recent headlines show NATO nations stepping up with renewed commitments to increase defence spending, while the US has also reaffirmed its commitment to NATO – an encouraging signal of stronger collective resolve.

Funding remains a challenge, and the 2035 aspiration to reach 5% of GDP in defence spending will require difficult choices to be made and sustained political will. Europe must rebuild its defence manufacturing base, which has been hollowed out by decades of peace. Long-term investment – not short-term procurement cycles – is vital, and private capital will be required to support defence innovation.

At the same time, regulatory reform is needed to streamline defence procurement processes and improve responsiveness to urgent needs. Current European stockpiles remain insufficient for a prolonged conflict, underscoring NATO’s need to prepare seriously for the possibility of war within the next two years.

In closing, General Borton warned that the West faces a determined adversary in Putin and that deterrence must be restored through strength and unity. He reminded the audience of Churchill’s famous rebuke of appeasement: “You were given the choice between dishonour and war. You chose dishonour, and you will have war.”

The change is seismic. Having experienced a long period during which Germany and many other European countries gave low priority to defence spending, recent developments have been striking. Finland and historically neutral Sweden have rushed to join NATO, while Norway now allows its $1.8 trillion sovereign wealth fund to invest more openly in defence initiatives. Meanwhile, Germany has also announced a huge boost to spending – both on defence, infrastructure, and a more general fiscal stimulus.

In addition to defence as an obvious point of focus – which has already seen the share price of a number of companies leap – there are wider implications for this rise in spending. Germany’s vast fiscal measures amount to a few percentage points’ extra spending into the economy, including a €500bn infrastructure fund with further growth initiatives on top. This is monumental as far as the Eurozone is concerned. There appears to be a clear willingness to boost economies fiscally, as opposed to relying solely on interest rate stimulus through the European Central Bank.

It is appropriate then, given the recent American stock market experience, that we consider this change in our investment outlook and in screening for potential investment opportunities. It should also be noted that, as a house, we have already been running a significant position in European equities for some time, largely based on more attractive valuations. The starting point, therefore, is appealing.

When faced with such a fundamental change in the outlook, as any practiced chess player would, McInroy & Wood takes time to consider the implications of such transformation – attempting to identify the areas of more structural, longer-term strength, as opposed to following, perhaps, shorter-term, knee-jerk stock market reactions. We seek to think ahead.

Our investment preference has always been to root out the ‘picks and shovels’ – those companies that supply an industry or benefit from structural growth in spending or activity. Seeing this jump in extra spending going into an economy will boost employment levels, consumer spending, infrastructure, confidence and so on; the continent appears likely to see a well-timed lift.

We watch the unfolding landscape with deep interest.

The views expressed in this article are not intended as an offer or solicitation for the purchase or sale of any investment or financial instrument. The information contained in the article is fact based and does not constitute investment research, investment advice or a personal recommendation, and should not be used as the basis for any investment decision. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. This article does not take account of any potential investor’s investment objectives, particular needs or financial situation. This article reflects its author’s opinions at the date of publication only, the opinions are subject to change without notice and McInroy & Wood shall bear no responsibility for the opinions offered.

Markets don't like uncertainty - and right now there is plenty of it. Conflict in the Middle East, questions over oil supplies and renewed tariff tensions have all tested investor confidence. How are our clients’ portfolios positioned for this environment, any why?

ESG investing and the energy transition have failed to reduce global carbon emissions over the last decade. What factors have slowed the energy transition? And how should investors prepare for the next ten years?

Doing the right thing in investment markets usually feels unpalatable. Finding value often means swimming against the tide and hunting for ideas where others are not.