Our Harrogate office recently hosted a guest speaker event, where energy expert Graham Cooley gave a talk on the UK Energy Transition, asking the question ‘Is full electrification the answer to decarbonisation?’ Graham outlined where the UK sits in this evolution, as well as some of the threats and issues that need to be addressed.

Graham is incredibly well qualified academically to talk on the subject, with a PhD in Material Physics as well as an MBA and is an Honorary Professor at Brunel University amongst other accolades. He also has vast experience in the corporate world, having been CEO of several companies in addition to helping many younger businesses, both as an investor and non-executive director, in public and private markets.

The presentation opened with the proposition that we are now firmly in the ‘Fourth Industrial Revolution’ that is attempting to move the world to a ‘net zero’ position by 2050. A key difference to previous revolutions powered by coal, oil, and gas, is this one is driven not by fossil fuels, but by equipment that harnesses renewable energy such as wind, solar, and tidal power. Success in this transition will depend on investment in such equipment.

The UK has genuinely made progress towards net zero and is amongst the leaders. Electricity generation from fossil fuels has halved in the past decade. Meanwhile, energy from renewable sources has more than doubled and power generated by wind is now equivalent to that produced from gas. Capital investment has been essential in building the necessary renewable infrastructure, but once the turbines are operating the production of energy should be cheap. The first conundrum, then, is why haven’t energy prices fallen?

The main reason lies in how energy prices are set: they are determined by the most expensive form of production currently in use, which is typically gas. While renewable sources such as wind and solar are becoming more prevalent, they are inherently intermittent – the wind doesn’t always blow, and the sun certainly doesn’t shine all day, especially not here in Yorkshire. Such intermittency means they are not best suited to meet our continuous demand for power, and our desire to switch on the lights at any time. Gas-fired power stations can be brought to life in minutes and are used to meet shortfalls, in addition to providing a base level of power. But this comes at a cost.

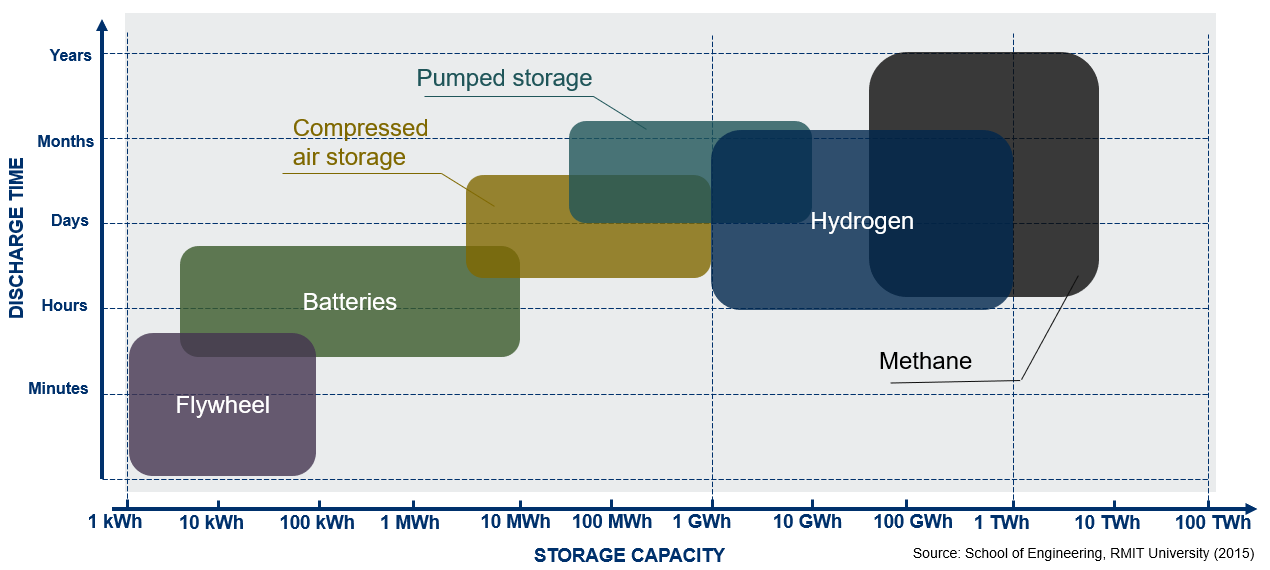

It is during storage that we need to separate the idea of electrons and molecules. When energy is produced and used, it is in the form of electrons. However, we can only store energy when it is in the form of molecules, either in fossil fuels such as coal, oil or gas, or from renewables such as hydrogen. The storage scale relates to how long you wish to hold power for. Batteries suit a short-term position, either Lithium-Ion for a few hours or Flow Batteries for up to a day. Longer term storage requires a different approach.

Hydrogen is a desirable fuel – any GCSE Chemistry student will know that its symbol is H₂, meaning it contains no carbon. That absence of carbon makes it an environmentally friendly option. Once energy is converted into molecular form, such as hydrogen, it can be stored for long periods or transported to where it’s needed.

This is where the infrastructure investment is needed, and in a different form to previous industrial evolution. Where before we typically burnt the molecules to generate electrons, we now seek to use electrons to create the molecules via investment in equipment, perhaps a turbine or solar cell. A wind turbine generates the power – that may pass through a ‘hydrogen electrolyser’ to create ‘green hydrogen’ and water – we may then store the hydrogen to use later. It is the investment in this new equipment that is now needed.

Funding this level of investment requires a concerted effort, as the sums involved are substantial. This isn’t a matter of simply securing a loan from the local bank – it calls for a broader industrial strategy, ideally led by government policy and supported by capital markets. Many of the businesses operating in this space are relatively small or early-stage, meaning they may not yet be profitable or widely represented in market indices. As such, investors will need to rediscover an appetite for selective risk-taking, seeking out long-term returns through active investment, rather than relying solely on passive strategies that track indices and benchmarks. This would mark a shift from the dominant investment flows of recent years.

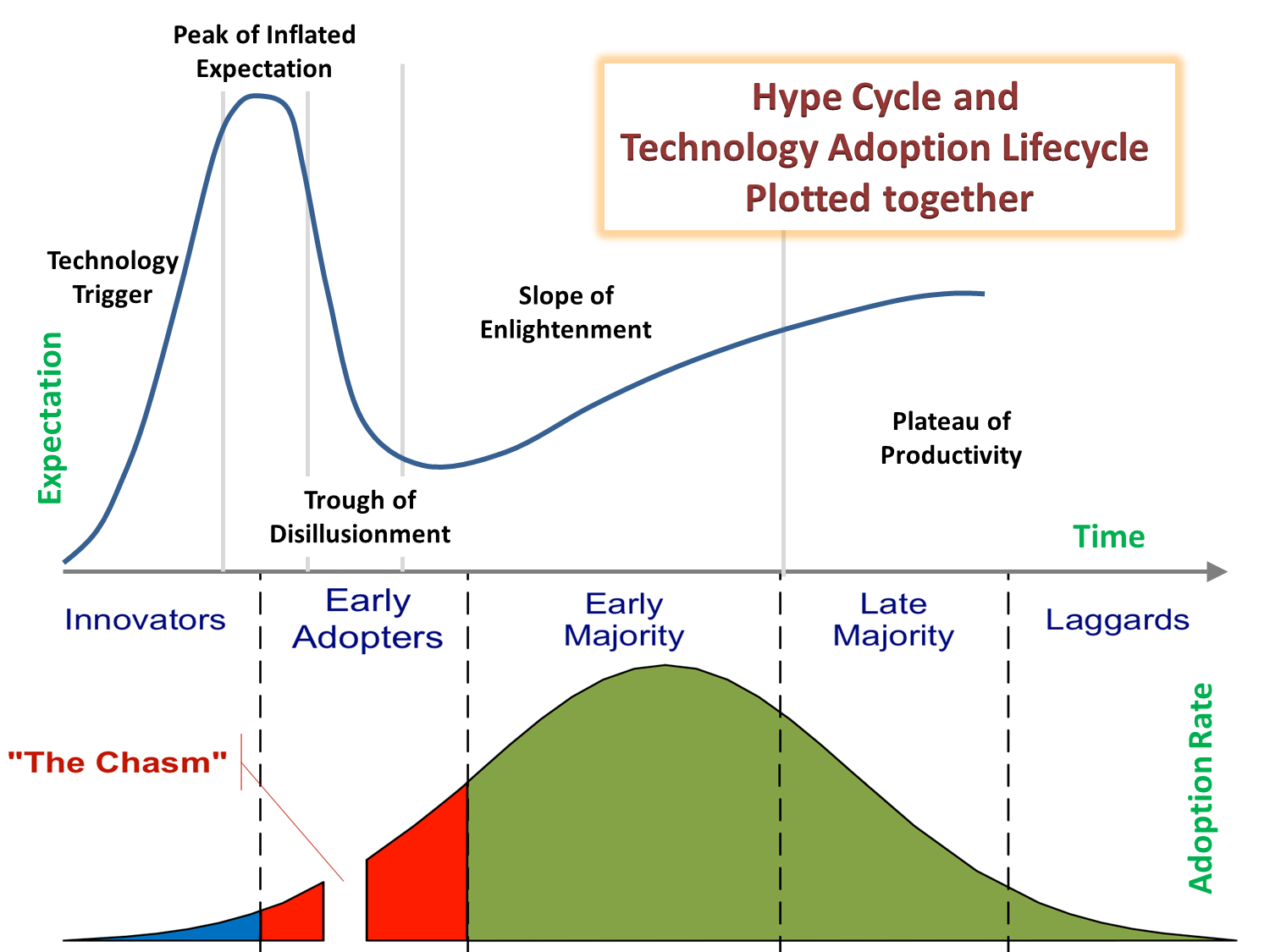

A great chart supporting Graham’s argument that whilst it may feel difficult to look at this space to invest, it is such periods that may give way to exciting returns – the ‘Trough of Disillusionment’ is the point that we have reached.

Source: Gartner

MW has invested in this space for some time and has selected companies across the size and technology spectrum.

A strong example of this is French company Air Liquide - a market leading manufacturer in the global industrial and healthcare gases sectors. While the company has demonstrated strong pricing power and a healthy dividend track record, it is one of the more carbon-intensive businesses within our preferred list of companies. As a result, we regularly engage with the management team regarding their environmental strategies.

The company aims to invest around €5bn in energy transition projects between 2022 and 2026, which equates to about half of their non-acquisition related investment over that period. Projects include hydrogen mobility (such as a joint venture with TotalEnergies to build and operate hydrogen filling stations for HGVs across Europe) carbon capture, and decarbonisation of the steel and chemicals industries. Air Liquide have also committed to investing €8bn between now and 2035 in the hydrogen supply chain, which includes electrolysers for the production of green hydrogen.

Graham exhibited some frustration with the UK government’s current drive to ‘electrify everything’ as a solution to our net zero dilemma. His contention is that even with our moves to grow our renewable power generation, there is a far larger opportunity elsewhere in the economy – heating. Electrifying more of our homes will require more roads to be dug up, more copper to be supplied, and infrastructure to be built, which will be both costly and time consuming.

A more attractive long-term proposition is to convert this power into a form that can be stored and then used via existing infrastructure. This approach offers the dual benefit of significantly reducing emissions while making use of systems already in place, potentially delivering the transition at a fraction of the cost—and ultimately helping to lower energy prices.

Most of our homes, offices and factories however already have a gas pipe! So, why not repurpose this system to distribute hydrogen? Using our GCSE Chemistry again, the gas currently flowing into homes is CH₄ (methane) where the C is carbon. Replacing methane with hydrogen (H₂), which contains no carbon, could drastically cut emissions from heating. With only modest adjustments to the existing network, this could prove a faster, cheaper, and more practical route to decarbonising heat – one that aligns with both environmental goals and economic realities.

The views expressed in this article are not intended as an offer or solicitation for the purchase or sale of any investment or financial instrument. The information contained in the article is fact based and does not constitute investment research, investment advice or a personal recommendation, and should not be used as the basis for any investment decision. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. This article does not take account of any potential investor’s investment objectives, particular needs or financial situation. This article reflects its author’s opinions at the date of publication only, the opinions are subject to change without notice and McInroy & Wood shall bear no responsibility for the opinions offered.

We explore this deceptively simple question, examining the cognitive trap of judging decisions by their short-term outcomes rather than the quality of the process behind them.

Markets don't like uncertainty - and right now there is plenty of it. Conflict in the Middle East, questions over oil supplies and renewed tariff tensions have all tested investor confidence. How are our clients’ portfolios positioned for this environment, any why?

ESG investing and the energy transition have failed to reduce global carbon emissions over the last decade. What factors have slowed the energy transition? And how should investors prepare for the next ten years?